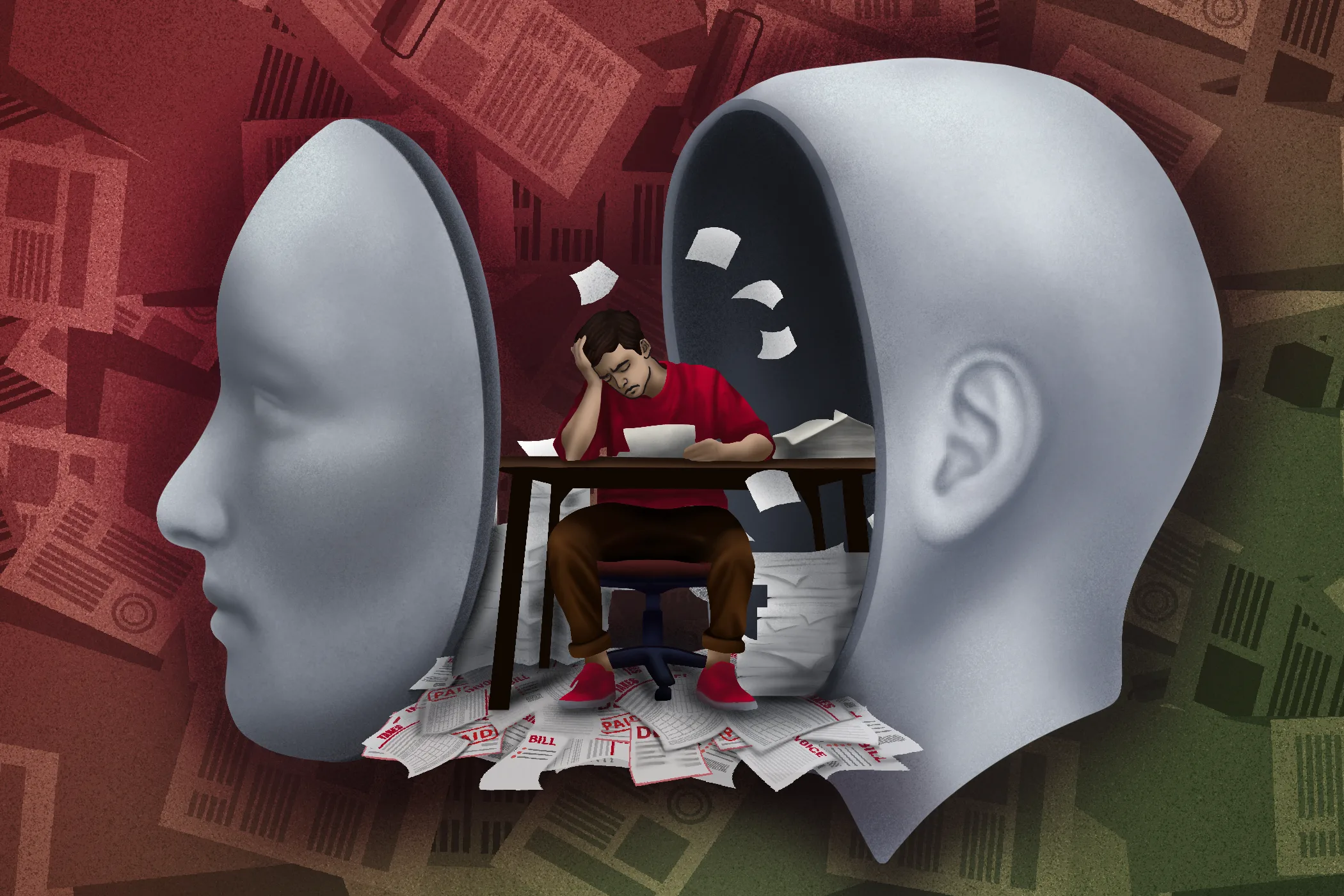

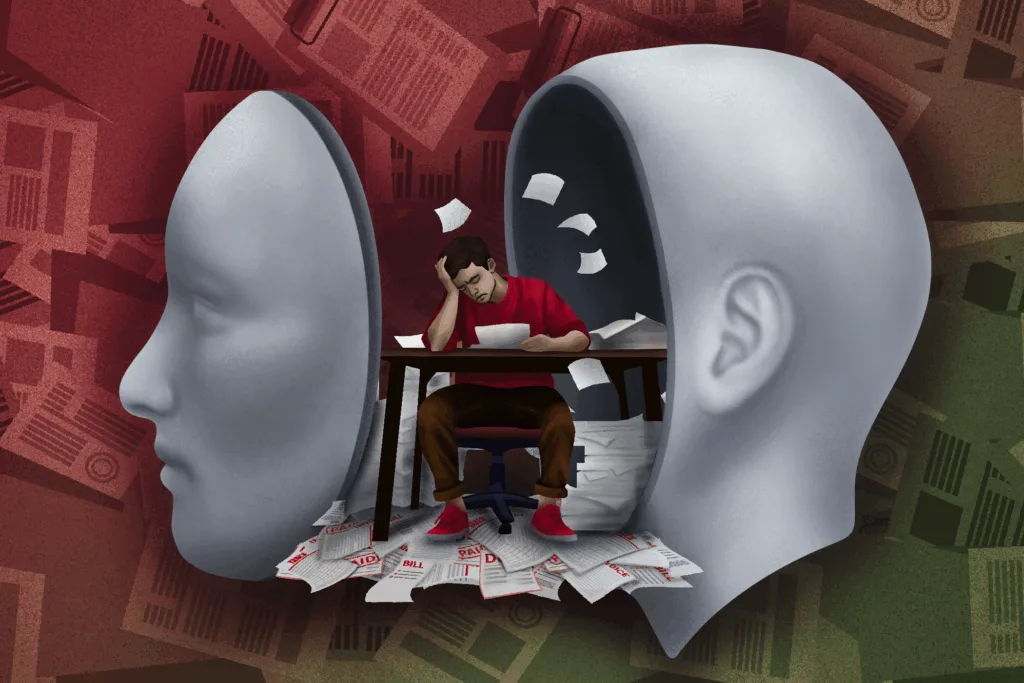

For countless young individuals, financial pressure involves more than mere repayment strategies and interest rates. It can lead to significant mental health struggles.

Gaurav Sinha, an assistant professor at the University of Georgia’s School of Social Work, is delving into the complex relationship between mental wellness and financial stability, especially in young adults.

Sinha’s investigation illustrates a daunting reality. The weight of debt, particularly among those aged 18 to 34, can initiate a range of mental health challenges, from stress and anxiety to profound depression.

Social Causation Versus Social Drift

Central to Sinha’s study are two primary competing sociological theories. One is termed social causation, while the other is known as social drift.

Social causation posits that being in a state of poverty or low socioeconomic status directly results in mental health complications. In contrast, social drift theory, or social selection, suggests the reverse—that a decline in mental health leads individuals to drift into financial hardship. Sinha examines the interplay of both theories.

“Debt and mental wellness influence one another in a cyclical manner,” Sinha explains. “It forms a feedback loop. Those with mental health challenges may find their conditions exacerbated by financial strain, and the funds they might allocate to their mental health concerns contribute to accumulating debts.”

Sinha asserts that both social causation and social drift are concurrently at play among contemporary youth. An increasing number of students are encumbered with substantial debt even prior to graduation. The Education Data Initiative indicated that the national federal student loan balance was $1.693 trillion in 2025, impacting 42.7 million borrowers repaying their federal loans.

“Research indicates that among these student debt holders, one observes heightened stress, anxiety, and diminished self-worth, alongside severe mental health conditions such as depression,” Sinha states.

Why is Financial Literacy Essential?

What’s fueling this crisis? A significant finding in Sinha’s research highlights the lack of financial awareness among young individuals.

“Upon turning 18, individuals can suddenly acquire various forms of debt,” Sinha remarks. “Credit cards, car loans, student loans—many emerging adults may not even know the right questions to pose, let alone what interest rates to consider or how to handle their loans.”

A 2023 survey by the TIAA Institute revealed that numerous Americans experience inadequate financial literacy. On average, adults could correctly answer only 48% of the survey inquiries, a clear indication that many are unprepared to make informed financial choices.

This gap in knowledge can render every financial choice daunting. For those already grappling with significant mental health concerns, the pressure intensifies. Sinha refers to it as “cognitive and affective burdens,” the mental exhaust caused by continuous anxiety and uncertainty.

Sinha strongly contends that combating financial stress begins with education. He advocates for customized financial literacy initiatives, particularly aimed at young individuals navigating student loans and wishing to deepen their understanding of their obligations.

From concealed fees in car loans to credit card snares, Sinha advises young adults to scrutinize the details and base their decisions on sound knowledge.

“If someone presents you with a new car for $100 monthly, it may seem appealing,” he cautions. “However, investigate further. Is the interest rate elevated? Are the conditions less favorable? Grasping these elements is vital.”

When Sinha embarked on this research over two decades ago, he collaborated with low-income families living paycheck to paycheck, at a time when many didn’t even possess a bank account.

“Numerous low-income families felt angry, anxious, or despondent regarding their financial situations. I wanted to discover if there was anything I could do to assist, and that’s how this research commenced. Hence, it’s particularly significant,” Sinha explains.

Financial Planning Can Transform Your Future

Sinha encourages students and young adults to engage in open discussions—with counselors, friends, family, or financial experts—and to seek support when necessary.

“Young individuals are powering the global economic engine,” Sinha observes. “By equipping them with financial acumen and supporting their mental welfare, they can become more productive and better individuals. Who wouldn’t desire that?”

He states that the initial step is to acknowledge the existing debt. The second step is to recognize that seeking assistance is not a weakness but a crucial method of managing both mental health and financial anxiety.

Consulting with someone may alleviate your mental strain or direct you to resources previously unknown. Whether that individual is a family member, a therapist, or a banker, inquire before making any significant decisions. Once you have clarity on your goals and have established a support network, numerous resources for debt relief and financial planning are available:

- The Office of Federal Student Aid’s loan simulator assists in estimating monthly payments and forecasting their effects on personal finances.

- UGA Extension’s online tools feature articles on managing debt and maintaining good credit.

- State-Specific loan forgiveness initiatives provide relief for individuals in specific professions like healthcare and legal fields.

“Debt does not define who you are,” Sinha asserts. “It’s undoubtedly challenging, but it can be managed. What truly matters is you. You matter. Your mental health is important. Your life holds value. Don’t allow debt to diminish that.”

The post How Financial Stress Affects Mental Health appeared first on UGA Today.